Sign In

Sign In 0 Items (

0 Items ( Search

Search

A friend in funds management in Sydney sent me an email last weekend which said in part that special interest groups “will not be receiving government funding for much longer. The outlook for the Australian economy is nothing short of frightening. We have utterly squandered a one-in-a-hundred year economic boom.”

A friend in funds management in Sydney sent me an email last weekend which said in part that special interest groups “will not be receiving government funding for much longer. The outlook for the Australian economy is nothing short of frightening. We have utterly squandered a one-in-a-hundred year economic boom.”

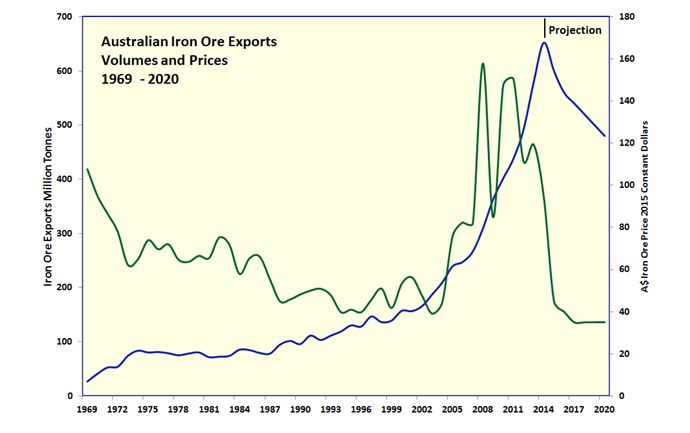

Yes, a lot of people are now running around saying that the sky is falling, but how far could it fall? Let’s have a look at iron ore. The chart following shows Australian iron exports and prices from 1969 with a projection to 2020. The prices are in 2015 constant Australian dollars. Iron ore volumes are the blue line and prices are the green line:

Iron ore exports took off in the 1960s with the Japanese steel boom then hit a brick wall with the first oil price shock of 1973. There was a 14% volume decline from 1974 to 1981. The iron ore price entered a gentle long term decline from the early 1970s, losing about 30% of its value and bottoming out in the 1990s, even as export volumes were rising. There was a price dip in 2003 even as export volumes started to accelerate away at the beginning of the China boom. The chart shows a volume contraction of 24% from now to 2020. In the Japanese steel boom of the early 1970s, production capacity peaked at 140 million tonnes per annum, production peaked at 120 million tonnes per annum and then fell to 100 million tonnes per annum. A contraction of a similar magnitude could be expected in China.

What determines how much money we make out of digging up iron ore though is the price. Some people think that the price will hang around the current level of US$60 per tonne. But if we look back twelve years ago, the price was $39 per tonne (in current day dollars) and that was a tight market. The Chinese steel producers say that their production will not be increasing from the current level. More supply is coming on from Australia though. There will be a price response to clear the oversupply. My chart has the iron ore price bottoming at $35 per tonne which is a few dollars per tonne less than what it was trading for in the 1990s in 2015 dollar terms.

The two big producers, BHP and Rio Tinto, have cash operating costs, that is not including depreciation, of about US$20 per tonne. Let’s use that figure to make a stab at the notional free cash flow that Australia has generated from iron ore exports from 2000. The chart following shows the result.

Early last decade, Australia didn’t make much money out of digging up iron ore. The golden years were the five years of 2010 to 2014 when we were making $40 to $50 billion a year that was used to pay taxes, dividends, boom-era wages and investing in building more iron ore mines. A couple of years ago, resources construction peaked at 7% of the economy.

We got used to living with an extra $50 billion a year odd from iron ore and now we are going to have to adjust to living without it. It is a similar story with coal. The Federal Government has told us to tighten our belts but hasn’t acted as if it meant it. The West Australian Government ran up $30 billion-odd of debt during the iron ore boom and is having one last splash of vanity projects with billion dollar price tags. You know how it will all end.

David Archibald, a visiting fellow at the Institute of World Politics in Washington, D.C., is the author of Twilight of Abundance (Regnery, 2014)

I can tell you exactly when the end came. It was September 2012. The mining consultancy industry, a bellwether for the industry as a whole, simply disintegrated in that month. It was like a nuclear explosion in its speed and intensity. The entire industry as a collective flicked the kill switch on all spending. Since then there has been no improvement; none whatsoever, and we are into the 3rd year of Armageddon. The professional knowledge and skills drain within the industry has been catastrophic.

Mine sites are already beginning to show signs of atrophy as people become jaded, cemented into often unsatisfactory roles. They are laden with inexperienced staff, operators and management who are bamboozled about what to do next, because the most skilled and experienced were generally in advisory or corporate roles which are long gone. This was the second part of the double whammy to the knowledge base, after skill were traded down during the boom.

There is now enormous under/unemployment in the industry, which is in no way reflected in national unemployment figures. Think in multiples of 10, not single digits.

Those of us with skin in the game understand the boom and bust cycle. We saw a monster boom, but the cataclysmic bust we are enduring now has shocked everyone. The big players – iron ore and thermal coal – look to be in a long term decline. There is still some hope that base metals and gold will keep the industry rolling.

I live in the Hunter which is, of course, key to the resources sector. The real estate market has plummeted here and there are a great number of properties for sale over $850,000 as people try to re-calibrate their financial commitments. I’ve lived in the Hunter since 1979 and could have told everybody that the boom and bust cycles are part of the paradigm and the latest downturn was totally predictable. Meanwhile, Sydney forges ahead with unprecedented real estate growth and the rest of the country goes backward. Forward planning is key; those who studied Geology at university within the last few years will not be unemployed. Time to re-train!!