Sign In

Sign In 0 Items (

0 Items ( Search

Search

Economists do little harm outside of government. True, the Sydney-based Australian Bankers’ Association Research Directorate was closed down shortly after I left my position of economic adviser in the mid-1980s, and the State Bank Victoria collapsed while I was chief economist at the beginning of the 1990s. However, I protest my innocence and impotence. I was too uninfluential to be instrumental in defining events. And, let me say, most economists in the private sector are in the same boat. That’s not the case when it comes to government. When in government, and most definitely I include central banks as part of government, there is no limit to the damage economists can do. We are about to live through a time which underscores that baleful reality.

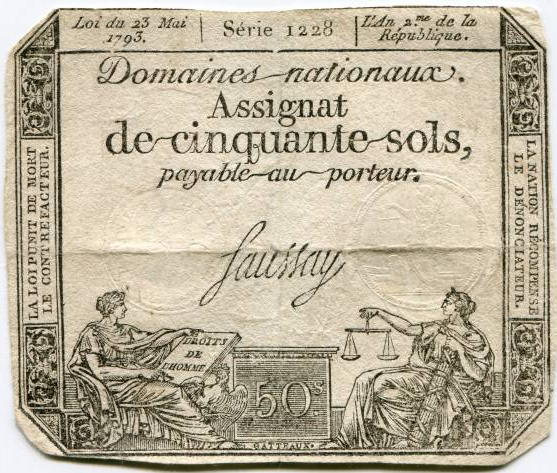

Inflation has been let loose. This has not been the product of happenchance, unforeseeable by those trained in economics or, in fact, by anyone with the slightest interest in economic history. Inflation (a persistent and appreciable rise in the general level of prices) has a long history. One episode which especially piques my interest took place in revolutionary France. It is interesting not simply as an example of inflation but because the powers that be back then, in 1789, acknowledged that issuing paper money (“assignats”) was a risky, inflationary idea.

Florin Aftalion (in The French Revolution: An Economic Interpretation) quotes Count Mirabeau, who saw the problem while trying to put something of a gloss on it:

I would agree with those who describe such an issue as a theft or a loan at sword-point but I would also allow that, in exceptionally critical circumstances, a nation may be forced to have recourse to bills of state. One should banish from the language the infamous term paper money … Under any other circumstances, all paper money is an offence to good faith and to the nation’s liberty; in its circulation, it is a kind of plague.

The plan was to temporarily issue assignats (pictured atop this page), which would be redeemed (and burnt) through the sale of public lands, mostly confiscated church property. The French chemist Antoine Lavoisier, a few years before his untimely guillotined end, demonstrated that church property was worth only 1,050 million assignats against the plan at the time to issue 2,000 million. It would bring about an “increase in value of all things”, he said perceptively, also in 1789.

Alas, the appetite for issuing assignats proved too strong. Up went the price of bread and everything else. According to William Doyle (in The Oxford History of the French Revolution), “a nominal 45 billion livres worth of paper was issued between 1790 and 1797, but its total real value (at 1790 prices) was less than a seventh of that.” We are not in that hyper-inflationary league. Nevertheless, the principle applies. Drop too much money into an economy and abracadabra, inflation appears; and not by magic. If Mirabeau and Lavoisier, among others, knew that in 1789 then I don’t think the Reserve Bank’s governor, Philip Lowe, or the Fed’s Jerome Powell or the Bank of England’s Andrew Bailey can profess ignorance of what causes inflation. Yet inflation is what we have. And no one has resigned.

Personally, I don’t think we should be so forgiving of million-dollar-plus-earning potentate economists who royally mess up the very task that they are principally employed and generously paid to get done right. But let me start by giving them the benefit of an excuse of sorts, as a curtain-raiser to my main objective. Not to put too fine a point on it, that objective is to explain why central bankers have bungled and botched their jobs. As I will show, their focus has been, and is, on the wrong economic variable. Another instance of being led astray by the error-strewn Keynesian script.

To the curtain-raiser. Whatever dreadful plight you’re in, it is better to have company. Lost in a wood; better with mates. First, you might be able to share the blame for taking the wrong fork in the path. Second, the baying sounds around you are less frightening than they would be if you were alone. Importantly, everyone has seen those horror movies where those lost split up to find help or a way out. Never a good idea. So it is that the allure of sticking with the crowd partly explains the wrong turns taken collectively in recent times by central banks.

One Australian newspaper headline read, “Costello blasts RBA’s failure”. Another: “RBA under the pump on inflation”. Same kind of the thing in the UK Telegraph: “The Bank of England’s credibility is now severely compromised”. And in the United States, the former Chair of the Fed got into the act: “Bernanke says the Fed’s slow response to inflation was a mistake”.

All of the above comments and many more were made in May and June, when central banks eventually woke up to the fact that the rise in inflation after the end of Covid lockdowns might not be transitory after all. Notice that their enlightenment came en masse. This is not surprising. Their antennas are always pointing in the direction of their international counterparts.

No (first-world) central bank wants to stand out from the crowd. Thus, each can be caught up in the swell—and, to boot, without quite knowing its origin. Often it begins with a consensus built on conventional economic theory. For example, times were tough during and immediately after the recession of 2009-10. Theory pointed to the need for central banks to force interest rates lower. They acted accordingly, more or less in unison. From there, each kept a weather eye on what the others were doing.

No central bank wants to keep interest rates materially lower than its counterpart central banks. Doing so might well reduce the value of its country’s currency and, thereby, cause untoward price rises; initially in imported goods and services. None wants to materially tighten ahead of the rest for fear it will increase the value of its country’s currency and cause additional unemployment; initially in export and import-competing sectors. So, each one is stuck until a new consensus develops. Meanwhile they have the comfort, when things go awry, of being in the same pickle. They can form a laager to counter “untutored” criticisms from those not holding the secret knowledge. And they can find solace in sharing each other’s plight.

This essay appears in September’s Quadrant.

Click here to subscribe and avoid the paywall

None of this implicit collusion would matter if their economic script were sound. They’d move in unison in broadly the right direction. Unfortunately, their Keynesian-derived script is unsound, which brings me to why things have gone wrong. Incidentally, be in no doubt, things have gone badly wrong. Inflation is the worst of economic ills. Incompetence has been at work, akin to pilot error. Though, there’s the difference that pilots face punitive consequences.

Inflation clouds price signals and in so doing complicates investment decision-making. It brings undue enrichment to some (such as wealthy owners of real property) and undue impoverishment to others (such as pensioners with cash savings). And that’s before the “fun” begins, when central bankers hike interest rates to quell the inflation which they’ve previously fuelled.

Hikes in interest rates shock the economic system. The patterns of resource allocation, and borrowing and spending, fitted for low interest rates are suddenly ill-fitted for the new regime. The result is economic distress (for example, for those with large mortgages) and increased unemployment (for example, among those working for heavily-geared businesses). Full-blown recessions can result—not a small thing. It can’t be described as a minor lapse on the part of those charged with preventing inflation in the first place.

It’s best, I believe, to go to Milton Friedman to discover why things have gone wrong. My own choice of Friedman’s extensive writing on monetary economics is his easy-to-read book Free to Choose, first published in 1979, which he wrote with his wife Rose. It’s a marvel of clarity and plain common sense. Common sense because much of economics is common sense when stripped of technical-cum-mathematical embroidery. Look at one of the most foundational concepts in economics; namely, the downward sloping demand curve. It simply says that when the price of a good goes up the demand for it usually goes down, and vice versa. Who in the world wouldn’t reach that conclusion? No economics textbook required.

Friedman promotes a concept which is analogous to the downward sloping demand curve. It is that the more money there is around, the lower its value is likely to be in term of the goods and services each unit of money can buy. The more seashells on the desert island, the fewer the number of fish ten shells can buy. Makes sense. Correspondingly, the more seashells, the higher the price in seashells of each fish. Suppose a giant wave were to hit the island bringing, in its aftermath, a great abundance of seashells. Then the price of each fish would soar. Inflation would hit the island.

The well-known equation MV=PT provides a frame of reference. Equations can be daunting. Relax. This one isn’t.

What it’s saying is that the number of times (V) each unit of money is passed from hand-to-hand times the number of units of money in circulation (M), equals the turnover (T) of goods times their price (P). It’s a truism, an identity. However, it becomes meaningful when it is assumed, as does Friedman, that the value of V is broadly stable, measured over a complete economic cycle. Then an increase in the money supply beyond the rate of increase in production (tied one-to-one with turnover) translates, indubitably, into a rise in prices; and, voila, we have the Quantity Theory of Money. In a nutshell: increases in the money supply beyond increases in real production engender increases in the general level of prices.

Contention surrounds the stability or otherwise of V; the so-called velocity of circulation of money. Keynes in the General Theory considered it to be a “will-o’-the-wisp” and, therefore, entirely unpredictable. If that were so, there would be no way to predict the effect of changes in the money supply on production or prices. Thus, he focused on interest rates as the pivotal factor in determining the pace of economic activity; a first-order error, bequeathed to central bankers.

The behaviour of velocity is an empirical question, which Friedman answered through exhaustive examinations of data. The prime example is his Monetary History of the United States, 1867–1960. But in Free to Choose he looked at data from Germany, Japan, the UK and Brazil. Everywhere he looked, the money supply and prices rose closely together, with price inflation lagging behind excessive monetary growth by some twelve months or so. Hence his familiar conclusion that “inflation is always and everywhere a monetary phenomenon”.

A highly correlated positive relationship between money and prices means, ipso facto, that the velocity of circulation of money is relatively stable. Otherwise, the close relationship would be undone. QED? Well, perhaps not for Keynesians, or their Modern Monetary Theory cousins, as I explained in “Unmasking Modern Monetary Theory” (Quadrant, July 2019). It would queer their pitch when advocating a combination of deficit spending and low interest rates. It’s time to get a little interrogative with money and its use. Bear with me. It strikes at the flawed thinking of central banks.

Money has various definitions. A narrow one of cash plus at-demand deposits in deposit-taking institutions (so-called M1 money) is the best, I think, when considering the velocity of circulation. This is the category of money principally used as a medium of exchange. However, when looking at some data below, I’ll use broader definitions for Australia and for the US to counter breaks in the series of narrow money. It doesn’t matter too much.

It’s a safe assumption that the amount of money that people and businesses hold to pay their bills is relatively unchanging in any given state of society. Evolution of new payment methods, such as credit cards, will change things to one extent or other. However, the state of the economy from one year to the next is unlikely to change the way money is used in the everyday business of buying and selling. At the same time, it’s recognised by Friedman, and more widely, that the velocity of money falls during economic downturns and rises during upturns. Pro-cyclical movements in velocity, it’s called. What’s going on?

In fact, the degree and the extent to which money is used for buying and selling don’t change. What changes is that during economic downturns extra money is demanded as a safe haven (fewer shares and more bank deposits). What is seen, therefore, as a fall in velocity is deceptive. The money being used for transactions is still turning over at the same rate. It’s just that a greater portion of the total supply of money is held aside; hoarded, if you like. The same reasoning applies in reverse during economic upturns, when velocity is seen to rise.

Take the situation during the recent lockdowns. Governments engaged in spending vast amounts of money to support individuals prevented from working and businesses prevented from operating. Governments sold bonds to fund their expenditure; obviously, increasing taxes wasn’t an option. Central banks set cash rates close to zero to keep interest rates down at the short end and bought up vast quantities of government bonds to keep longer-term rates subdued. The money supply jumped, as it was bound to do. Here’s a snapshot.

In Australia, M3 money, which includes demand and time deposits, increased by an annual 4.7 per cent on average from December 2015 to December 2019. In the following year, it increased by 12.6 per cent and in the year to December 2021 by another 9.3 per cent. Bear in mind too that the narrower definition of money would have likely spurted at an even greater rate in the two years to the end of 2021. (RBA figures)

In the UK, the average annual growth in M1 was 5.9 per cent between 2015 and 2019. In the following two years it averaged 13 per cent per annum. (OECD figures)

In the US, the average annual growth in M2, which includes demand and time deposits, was 5.5 per cent between 2015 and 2019. In the following two years it averaged 18.5 per cent per annum. (Fed figures)

Central bankers orchestrated large increases in the money supply. What did they think would happen? Did they think that the velocity of money would stay down to accommodate the untoward increases in the money supply; or could be safely disregarded as a will-o’-the-wisp, à la Keynes? I don’t know.

At first, the additional supplies of money were hoarded, as economies struggled and people and businesses were fearful of the outlook. Par for the course. But, at the beginning of 2022, once the outlook improved, these hoarded balances came into play—so to speak, from under the mattress into the marketplace. Procyclical velocity, it might be badged. Too much money chasing too few goods, is a more common or garden way of expressing it. And, as is usually the case, inflation is triggered by some untoward event—this time supply chain disruptions and rising energy prices, before the Ukraine conflict began, set inflation afoot. The Ukraine conflict added oil and gas to the fire; or, literally speaking, further constricted the supply of oil and gas. But, make no mistake, particular prices can rise because of, say, bottlenecks. Inflation cannot and will not occur in the absence of excessive growth in the money supply.

This inflation isn’t transitory; if there’s any such thing. By buying up government bonds, central banks allowed the money spent extravagantly by governments during the over-hyped pandemic to flood economies. Of course, there’s blame to share with governments and their treasury officials. Nonetheless, the onus in preventing inflation rests with central bankers.

Quantity matters. The sheer size of the bond buying sprees (quantitative easing on steroids) was the fault. Pushing interest rates down close to zero never makes sense. It’s much more damaging than it is helpful. It tends to encourage over-borrowing, not least on the part of governments. Setting the interest-rate hurdle too low encourages unproductive investments, including on home building. It sets up economies for painful readjustments when the chickens come home to roost, as they now are.

What to do? “That’s easy enough,” according to Friedman. “The government must increase the quantity of money less rapidly.” And he adds a cautionary note: “The most important device for mitigating the side effects [‘slower economic growth and higher than usual unemployment’] is to slow inflation gradually but steadily by a policy announced in advanced and adhered to so it becomes credible.” Why does he propose a gradual approach? In order “to give people time to readjust their arrangements”. Seems eminently sensible. Commonsensical, it might be said.

Go back to the period January to April in Australia. The cash rate is 0.1 per cent. Homebuyers line up for cheap housing loans, perhaps given confidence by earlier statements from the Reserve Bank that near-zero rates would last for a long time—to beyond the end of 2023, according to a media release dated November 2, 2021. From bad forecasting to reality: in May the cash rate is upped by 25 basis points, and in June, July and August by another 50 basis points each month, with more to come promised*. To wit: “The [Reserve Bank] Board expects to take further steps in the process of normalising monetary conditions over the months ahead …” Is this gradual, do you think? Or a tad sudden? Never mind, be thankful for small mercies. In the US, the Fed seems to have settled on jumps of 75 basis points.

Central banks appear to be intent on showing how tough and resolute they are in dealing with those who’ve irresponsibly overextended themselves. Or, more likely, are showing how panicked they are at having let the inflation genie out of the bottle.

I have no idea whether central banks are monitoring monetary growth. Friedman refers to the “Fed’s obsession with interest rates” rather than with “controlling the quantity of money”. Remember he wrote this in 1979. Nothing seems to have changed. The difficulty is that keeping interest rates too low resulted in excessive growth in the money supply and, inevitably, inflation. Making interest rates too high, too quickly, in the current circumstances, could result in a slew of bad debts, curtailment of bank lending and a corresponding collapse in monetary growth. Such a collapse would both reflect and presage more economic distress than is necessary or sensible to cure inflation. It might be termed getting it wrong on the way up and on the way down. With a nod to Oscar Wilde, to err on the way up may be regarded as ineptitude; to err also on the way down looks like delinquency.

* Promise fulfilled. Another 50 basis points on 6 September. Promise renewed. More to come.

Peter Smith is a frequent contributor to Quadrant and Quadrant Online

Thanks to Peter for this timely contribution on the aetiology of inflation and the uncritical, unquestioning herd mentality of our central bankers. This really is just an extension of the herd mentality that was a signature of all public institutions right throughout Covid and in regards to AGW. Once again, cool calm and collected reasoning has been replaced by a quasi religious belief in an overarching narrative fuelled more by emotion than logic. I think the role high energy prices, (brought about by AGW policies then exacerbated by Russia ) has played in this current bout of high inflation cannot be understated. Energy prices flow through to cost of all production and supply of services and have a even greater universal flow on effect on the economy than wages, which can be offset to a certain degree by shedding staff. With retail prices of energy yet to catch up with wholesale prices (up to 300% increase this year) and fuel excise to return to normal – there is a lot more inflationary pressures yet to flow through.

C K, people need to beware of the fact that Russia didn’t force Western Europe to go all green, decommission perfectly good power generating systems, and pay the price for Western Europe did it all by themselves. One way to cause the tears of laughter to course down the legs of the Russians, most Ruski Geophysicists and Geologists in particular, is to mention climate change or global warming. Our inept politicians have damaged our economy almost beyond repair and we taxpayers are the ones who will suffer because that’s where the money is. (apologies to Willie Sutton) The French note depicted above would be the equivalent of promissory notes issued in FNQ and probably elsewhere by companies after WW1 my grandparents spoke of as “shin plasters.” Keating was right about a banana republic more is the pity.

According to figures I have, US inflation was already 6.8% in November 2021, and had risen inexorably month after month since that March, from 2.6%. How is it possible runaway US inflation 18 months ago would not affect Australia at some point? Perhaps Blind Freddy should be appointed to the RBA?

Economics is politics- or is it the other way round? Under a Trump presidency, there’s no doubt. America is in recession. But under Biden…. ? And when the shit hits the fan on energy prices or whatever you can be sure the political/bureaucratic complex will find a way to tax the schmucks who fund the welfare state and give it to people who will keep them in the style to which they’ve become accustomed.BTW BOH above is entirely correct.

B O’H

>” … tears of laughter to course down the legs of the Russians, most Ruski Geophysicists and Geologists in particular, is to mention climate change or global warming”

Not just Russki geoscientists …

I was talking mundanely with a late middle-aged woman yesterday (inner-city denizen, she is) who literally could not say the word “coal” without a toned genuflection protective against the devil.

Quiet laughter is all we have. Green ideologues have destroyed us. Conjuring money by adding and infilling another column to the spreadsheets of the big banks (“printing” money) will make no difference to this.

The best example of fixing monetary problems was in Russia just after perestroika when the rouble went up and down like a roller blind. The exchange rate with the USD was about 5000 roubles to one USD so the “State” or whatever they called themselves simply cut the last two zeros from the rouble so that it became 50 roubles to the USD and the hardship was terrible to behold because that rate applied domestically as well as externally unlike our exchange rate that usually only affects imports.

Good piece Peter, thank you. I particularly like that formulae MV=PT. It’s a beauty, and puts things into a simple, and pretty obvious perspective with only a little thinking required.

Google the price history of a Can of Campbell’s condensed soup for a very interesting graph. From 1898 until about 1974 it is flat at 10c. From 1974 to today it rises, with a few fits and starts, to well over $1. (A 15% rise in only the last 12 months.) The product has remained the same so this price inflation corresponds to the devaluation of the purely fiat US dollar – it has lost 90% of its value. We have had the trickle and now the flood.

https://talkmarkets.com/content/us-markets/amazon-hikes-campbells-tomato-soup-prices?post=367997

And all this was also explained in “Yes, Prime Minister” when Bernard Woolley pointed out to the PM (Hacker) that Sir Frank as Secretary of Treasury had an even bigger problem than Sir Humphrey (Cabinet Secretary, who studied Classics at Oxford) in understanding the collapse of the Pound – he was an economist!

Yes Minister/Prime Minister; training films for public servants. Well worth boning up on.