Sign In

Sign In 0 Items (

0 Items ( Search

Search

The Global Financial Crisis through which the world recently passed was one of the most traumatic events in the world’s financial history. The world’s economic powerhouse, the United States of America, was shaken to its foundations. Banks collapsed in the hundreds, the government was forced to bail out its major investment banks at enormous cost, the country was plunged into recession and there was a run on the dollar. The Dow Jones industrial index, which had peaked at 14,198 in October 2007, crashed to 6,440 in March 2009, losing more than half its value. That fall was almost double the fall suffered by the same index after the attack on the Twin Towers in September 2001, which may be taken as proof that US investment banks can inflict twice as much damage on the USA as Osama bin Laden did.

The chaos spread. Britain had to nationalise part of its banking system, Europe’s economies and several of its leading banks suffered, Greece needed a €44 billion bailout from the International Monetary Fund and Iceland was effectively bankrupted. Confidence evaporated to such an extent that the world’s largest banks even stopped lending to each other.

Australia was on the periphery of the GFC but even so felt its impact. Municipal councils, particularly in New South Wales and Western Australia, had unwisely invested in toxic waste generated by US investment banks and consequently had substantial funds frozen, perhaps lost. The National Australia Bank, which had invested in similar toxic waste, took a $1 billion hit. Over-geared empires such as ABC Learning, Allco and Babcock & Brown collapsed. The ASX/S&P index hit a record 6,873 in November 2007 and more than halved to a low of 3,120 in March 2009. In early 2009 Australia was considered to be in recession by Prime Minister Kevin Rudd and the Governor of the Reserve Bank of Australia, Glenn Stevens: views which in hindsight were premature but which underlined the seriousness of the situation.

As the US and European economies now climb uncertainly out of the pit, the question arises of whether we risk a re-run of the GFC. To answer the question, it is necessary to look first at the factors which caused it.

The chain of events began with a fall in US house prices, which triggered defaults on US mortgages, which in turn led to bank collapses in the USA and Europe. US house prices had been in a bubble for a long time, and the reasons are instructive. Once upon a time, any financial institution which created a home mortgage kept that mortgage on its books. The institution, be it a bank or a savings-and-loan (known in the USA as “thrifts”), therefore had a strong incentive to ensure the mortgage was sound. And what is meant by “sound” is that mortgages were issued at a sensible discount to the value of the house and to borrowers who could demonstrably afford the repayments.

The soundness of mortgages was improved in the 1970s by the creation of the Government National Mortgage Association (“Ginnie Mae”), a government agency which guaranteed the mortgages of poorer home buyers. Later two further agencies were created to guarantee those mortgages which did not qualify for a Ginnie Mae guarantee. These latter agencies were the Federal Home Loan Mortgage Corporation (Freddie Mac) and the Federal National Mortgage Association (Fannie Mae). These three agencies had the government as the lender of last resort, so mortgages guaranteed by them had an implicit guarantee from the government itself.

US residential mortgages became one of the largest reservoirs of capital in the world’s largest economy. US investment banks eyed that pool greedily, itching to get their hands on it. But the reservoir was not a homogenous pool. Each mortgage had a different date of inception and termination. Each borrower was different and the homes varied widely in value. Interest rates differed. Also, US home borrowers had the right to terminate their mortgages early, which they frequently did so they could refinance the mortgages during periods of falling interest rates.

Salomon was the first large investment bank to try to deal seriously in mortgages, which seems to have been an initiative of a trader named Bill Simon, who went on to become Secretary of the US Treasury. Salomon traded individual mortgages, but until mortgages could be bundled together they could not reach the size necessary to interest the rest of Wall Street. In 1983 this feat was achieved at First Boston, reportedly by an executive named Larry Fink. First Boston created an instrument called a collateralised mortgage obligation (CMO). To make the example simple, let’s say a CMO comprised 300 mortgages with an average value of $US100,000, making the whole bundle worth $US30 million. The CMO would be divided into three tranches: top, mezzanine and bottom, worth $US10 million each.

Bankers who had been trying to evolve a way of packaging mortgages had long been stumped by the phenomenon of early repayment. A mortgage which had been drawn for thirty years might be repaid next month. How could you value such an instrument and—more seriously for Wall Street—how could you sell it to an investor?

The CMO hurdled this problem by defining mortgages in terms of time. The top (senior) tranche of a CMO would comprise whichever $US10 million mortgages were paid out first, either because they had been refinanced or expired naturally. The mezzanine tranche would comprise the next $US10 million and the bottom tranche would be the last $US10 million.

This structuring gave investors more certainty and safety. The CMO would contain only mortgages which had been guarantee by Ginnie Mae, Freddie Mac and Fannie Mae, which meant the investors were implicitly buying government-guaranteed paper. The income from the investment would be the interest rate on the mortgages, less whatever fees had been gouged out by the CMO’s promoters, and the term of the investment was roughly known. On average the mortgages in the top tranche would be paid out in three to five years, those in the second between five and fifteen years and those in the bottom up to thirty years.

The CMO was a brilliant invention. It freed up the books of home-lending institutions because they could sell their existing mortgages to make room for new ones. The CMO was also a new product investment that banks could sell to investors. Financial institutions such as mutual funds loved CMOs because, for the first time, they could make substantial investments in mortgages. As financial products are unpatentable, the First Boston CMOs were soon followed by a swathe of imitations, so a deep market developed in packaged mortgages.

But an innovation which brings benefits to the financial sector is not necessarily a benefit to the wider society. Like many inventions in human history, CMOs were a two-edged sword. As long as the mortgage originators had to hold the mortgages on their books, they were under pressure to husband their lending and monitor the subsequent performance of the borrowers. The fact that mortgage originators no longer had to hold mortgages on their books tempted them to lower lending standards. Each mortgage they wrote could now be shuffled on to a bank which in turn would shuffle it on to investors. The end investors might not know the identity of a single mortgage in their CMO, or care about them.

As previously mentioned, the early CMOs comprised only mortgages which had been guaranteed by the three government agencies and hence carried an implicit guarantee. Enter Bill Clinton. If we want to seek a villain responsible for undermining the credibility of the US mortgage, Bill Clinton is not a bad candidate.

This was a classic case of the road to hell being paved with good intentions. Clinton wanted to help poorer people to own homes. In 1993 Roberta Achtenberg, the lesbian activist who was assistant secretary for Fair Housing and Equal Opportunity at the Department of Housing and Urban Development, began implementing the Clinton agenda to “increase home ownership among the poor, and particularly among blacks and Hispanics”.1

The trend was accelerated when the Clinton administration made changes to the Community Reinvestment Act of 1977. Banks were rated on how much lending they did to low-income neighbourhoods. Simultaneously, Clinton slackened the rules governing Fannie Mae and Freddie Mac, pushing them to expand lending to borrowers who previously would not have qualified. The result was an 80 per cent increase in bank loans to low and moderate income families.

The first securitisation of sub-prime loans, for a total of $US385 million, was underwritten in October 1997 by Bear Stearns and First Union Capital Markets (later part of Wachovia and then Wells Fargo). The issue was a success, and so was followed by more.

Lending standards fell dramatically. Borrowers were offered low-start loans, interest-only loans and adjustable-rate mortgages. The low-start loans began with “teaser” rates which were artificially low but would be typically reset two years later. These low-start loans were delusionary because however cheaply they begin, the lender will need to get its money back at the right rate later on. At the end of two years, the rates were bound to be increased. Unless the borrower had improved his income by then, the loans could become unaffordable.

In the short term, the lenders didn’t give a hoot because they could flick the mortgages on to an investment bank which would repackage them and in turn flick them on to the fund manager of some institution. Everybody was happy. The borrower got a home, the lender made a fee, the investment bank probably made the biggest fee and the institution got a bundle of paper with a high credit rating earning a high interest rate.

The CMOs had by this time been almost phased out and replaced by collateralised debt obligations (CDOs). CDOs began as bundles of corporate debt which had been packaged and sold to investors. This article is purely concentrating on those CDOs which comprised only mortgages. For all practical purposes a mortgage-backed CDO is the same as a CMO, but as they were labelled CDOs we will refer to them as such from here on.

The US investment banks have a track record of making their “products” complex, to make it harder for their investors to value them or assess the risk. So CDOs morphed into increasingly more exotic instruments. The number of tranches could be as high as fifteen. Some were interest only, some principal only, and some were sliced and diced until the principal and interest repayments were on different mortgages. Principal repayments might be on Florida condominiums while the interest component was on houses in Arizona.

This raises the question of how the ratings agencies (Moody’s, Standard & Poor’s, and Fitch) managed to rate mortgages which were issued to increasingly less credit-worthy borrowers and bundled in more complex fashion. The answer takes us into mathematics and computer modelling. Credit ratings are differently styled by different agencies, but taking S&P as an example, they range from AAA for absolutely secure down to C which (my interpretation) means “this dog might not be around tomorrow”. A CDO might contain 100 entities, of which nineteen had a credit rating of AA or better, but the average rating was only A. However, the whole CDO was rated AA, above its average.2

How could this be? The answer is by an application of Galileo’s fourth law of probability. On S&P’s CDO evaluator, the probability of an A-rated company defaulting on its debts at some time within ten years was 3.041 per cent. Therefore the probability of two un-correlated A-rated entities failing would be 3.041 per cent x 3.041 per cent = 0.0011628 per cent. The probability of three such entities failing would be 3.041 per cent to the power of three, and so on. On this reasoning, the probability of enough entities defaulting to substantially reduce the value of the CDO was infinitesimal.

The crucial word in that paragraph was “uncorrelated”. The calculation would become less valid to the extent that there was a correlation between any of the entities in the CDO. The standard model for assessing this risk was inelegantly named the Gaussian Copula model.

Broadly, the modelling for correlation risk was based on the history of defaults by entities similar to those in the CDOs, and recent defaults were given a higher weighting than more distant ones. As house prices had been rising in the USA for a decade, the history of defaults was slight and this led to correlation risk being estimated as low.

A perfect example of Garbage In, Garbage Out. The modellers were aware of correlation risk, but the number of defaults in the sort of lists they were dealing with had been relatively rare in the past. The modellers therefore could not build a reliable model on the likely number of defaults in future. This leads us to a basic flaw in many computer models: the fact that an eventuality cannot be calculated accurately, sometimes not at all, doesn’t mean that it won’t happen. Modellers therefore tend to leave the incalculable out of their models.

It gets worse. In Michael Lewis’s book The Big Short, he claims that the credit-rating agencies were issuing their ratings on CDOs without having access to basic data on the mortgages. He cites the evidence of a former Standard & Poor’s sub-prime mortgage bond analyst named Frank Raiter, who gave evidence on October 22, 2008, to the Committee on Oversight and Government Reform. Raiter said the S&P managing director in charge of surveillance of sub-prime bonds “did not believe loan-level data was necessary”. Rainer produced an e-mail from S&P’s managing director of CDO ratings, Richard Gugliada, in which Gugliada said:

Any request for loan-level tapes is TOTALLY UNREASONABLE!! Most originators don’t have it and can’t provide it. Nevertheless we MUST produce a credit estimate … It is your responsibility to provide those credit estimates and your responsibility to devise some method to do so.3

The agencies collected fat fees from the investment banks for issuing the ratings.

So the CDOs were backed by apparently sound mathematics which gave them misleadingly high credit ratings. Salesmen for US investment banks, armed with these ratings, sold CDOs to the world.

It is worth noting that all this was happening in an unregulated market. The US share market is fairly heavily regulated, but the bond market is only lightly regulated and derivatives are for all practical purposes unregulated. Trading in CDOs was typically done between individual banks and institutions, and there was no listed market.

The buyers can be forgiven a little for not being able to analyse underlying data which wasn’t available to the rating agencies or even—according to the Gugliada email—to the mortgage originators. Only a handful of insiders really understood what was happening. Loans were increasingly being made to NINJAs (No Home, No Job, No Assets), who couldn’t even afford the first repayment. That didn’t matter, because as long as house prices were rising, unpaid interest could simply be capitalised as an addition to the mortgage.

Should the investment banks have done more due diligence before unloading these toxic mortgages onto customers? Certainly, but that does not seem to be the way US investment banks worked in the 2000s, or indeed for decades before.

Compared to Australia, the US banking system has been poorly structured. In the Great Depression of the 1930s, small US banks failed by the hundreds and their depositors were ruined. To avoid a repetition of this, the Glass–Steagall Act was introduced in 1933. Glass–Steagall separated commercial banks from investment banks. Depositors in commercial banks would henceforth be protected by the Federal Deposit Insurance Corporation. The price of this protection was that they were forbidden from underwriting and other speculative investment activity. The commercial banks were also, for most practical purposes, confined to single states and so never developed the branch networks we know in Australia.

The investment banks could underwrite issues and trade in speculative financial securities but could not take deposits from the public and were not protected from the FDIC. The investment banks at that time were private partnerships. If they went bankrupt, the losses were borne by the partners.

This situation prevailed until 1968 when Merrill Lynch changed from a partnership to a corporation. Then in 1970 Donaldson, Lufkin and Jenrette took the logical next step and offered shares to the public.

The rest of the investment banks followed. From then on, the executives who ran the investment banks were not risking their own money so much as that of their faceless shareholders. Greed and myopia took over. The chief executives overpaid themselves obscenely and took huge gambles. Shareholders and customers were regarded more as prey than as people who should be nurtured. Michael Lewis’s first book, Liar’s Poker, provides a searing snapshot of this world.

So mortgage issuers had become disconnected from mortgage holders, while investment banks had become disconnected from capital discipline. No private partnership would ever have geared itself 35:1 or bought and held $US50 billion in mezzanine CDOs, but US investment banks did in the 2000s.

Meanwhile, Glass–Steagall was under attack. The first crack was in 1998 when Citicorp bought Travelers, a large corporation that owned and controlled the investment bank Smith Barney. The $US70 billion merger was in breach of Glass–Steagall, so shouldn’t have been allowed to happen. Instead, the banking industry embarked on a lavish campaign to have Glass–Steagall repealed, which happened in 1999. The repeal act was signed by Bill Clinton. Clinton had a better grasp of financial history than most politicians and was wary of the repeal, but he signed it anyway.

Another important stepping stone towards the GFC was the grounding of the Exxon Valdez in Alaska in 1989. After the oil spill, Exxon had been threatened with a $US5 billion fine, which it covered by taking a $US4.8 billion line of credit with J.P. Morgan and Barclays.

Morgan had to offer the line because Exxon was a valued and long-standing customer. Morgan wanted to hedge its exposure, and the solution was found by a bright executive named Blythe Masters. She persuaded the European Bank for Reconstruction and Development to assume the risk on the line of credit in return for a yearly fee from Morgan. If Exxon defaulted, the EBRD would have to compensate Morgan for the loss, but if Exxon did not, the EBRD would receive a nice fee each year. Thus was born the credit default swap (CDS).

In principle, a credit default swap is insurance. The buyer of the swap is insuring itself against the risk that a company to which it is exposed might default. But as the CDS evolved, it became apparent that the buyer did not have to have a stake in the subject company at all. It could simply be a bet between two parties on the likelihood of a third party defaulting. The Exxon Valdez swap was done between parties who all understood the risks and rewards of what they were doing. But by the 2000s, CDSs were increasingly becoming gambling bets.

The CDS became a tool for a handful of canny investors who in the early 2000s realised that the US housing market was cracking and that the CDOs were increasingly being written on unsound mortgages. As Lewis relates in The Big Short, they decided the best way to short the housing market was to buy credit default swaps on mortgage-backed CDOs.

They researched the CDOs as far as they could and began buying CDSs against the CDO tranches which they regarded as the most likely to fail. The CDSs had to be bought from the banks that issued the CDOs. Typically the premium was 2 per cent, which meant the shorters would bet $US2 million a year on the possibility of a failure of $US100 million in CDO-tranched mortgages.

The investment banks appear to have held relatively little of the risk. The first credit default swaps were passed on to American International Group, which became the underwriter. As the world’s largest insurer, AIG was a natural underwriter, but this was pretty silly underwriting because the premia went as low as twelve basis points. A basis point is one hundredth of 1 per cent, so AIG might be selling $US1 billion of credit default swaps for a premium of a mere $1.2 million. Readers who have followed the story this far will have realised that there is no practical difference between holding a CDO and selling a credit default swap against it. In both cases a default will cause a loss of the same size.

Defaults on US mortgage payments began rising around the middle of 2006. Low-start loans appear to have been primarily responsible. Borrowers who took these loans were typically given a teaser rate for the first two years, after which the rate would be reset. As the lender has eventually to charge the right rate for its money, the reset would be a sharp rise in mortgage repayments—unless interest rates had fallen during the two years.

These teaser rates represented a low-risk strategy for investors. An investor could borrow at low rates for two years in the hope of reselling the house within that time at a profit. In the lax lending days of the early 2000s, an investor might have been able to borrow on several houses simultaneously. If the investor failed to sell the houses and the rates were reset to a level he couldn’t afford, he could simply leave the keys in the mailbox and walk away. Australian mortgages are normally loaned on the security of as many assets as the lender can obtain. In the USA, the security of a mortgage is normally on the house alone. This makes US mortgages riskier than Australian, because if house prices fall generally the lender is more exposed to loss.

The borrowers who took low-start loans in the halcyon days of 2004 were hitting reset shock in mid-2006 and started defaulting. It took a year for the US investment banks to grasp what was happening. A few sharp traders noted the trend on January 31, 2007, when the ABX index, a publicly traded index of Triple-B-rated sub-prime mortgage bonds, fell more than a point from 93.03 to 91.98.

The ABX was the tip of the iceberg, indicating what might be happening in the mortgage market and the CDOs derived from it. To the general public, the CDO market was invisible. Even in Wall Street, it took months before the penny really dropped. Then at the end of June 2007, Morgan Stanley and Goldman Sachs began unloading their credit default swaps.

In contrast, Bear Stearns had overstayed the market and was badly exposed. In June 2007, Bear Stearns terminated redemptions on two of its derivative funds. This created great nervousness, as it was unprecedented for a big US investment bank to be unable to fund redemptions of one of its own funds. Bear Stearns was having trouble raising cash to meet its obligations. Then in March 2008 it suffered a terminal run on its liquidity.

Bear Stearns was rescued by the President of the Federal Reserve Bank of New York, Tim Geithner, who underwrote a takeover of the bank by JPMorgan Chase at $US2 a share. The paperwork on the rushed deal was faulty, forcing the price to be upped to $US10 a share, but that must have been poor consolation to anyone who had bought them fourteen months earlier at their peak of $US172.

The markets grew increasingly nervous until September 14, when they reached a weekend that will go down in infamy. Between Friday, September 14, and Sunday, September 16:

- AIG had to be bailed out by the US Treasury;

- The US government bankrolled a takeover of Bank of America by Merrill Lynch; and

- Lehman Brothers died.

Panic ruled from then until the following March: six months which were the nadir of the Global Financial Crisis. Derivatives magnified the impact of the fall in US house prices. Not only did the mortgage-backed CDOs lose value, so did the credit default swaps. As CDOs went to zero, banks were faced with the prospect of paying out hundreds of millions to the buyers of CDSs.

As these were unregulated markets, nobody knew how many CDOs were out there or how many CDSs had been written against them—and it was possible for gamblers to have written a multiple of CDSs against any CDO.

The failure of Lehman took the panic to an even higher level, because Lehman had been the counter-party to countless swaps around the world. The buyers of these swaps now had no idea of when or whether they would be paid. Worse, the fact that one US investment bank had failed raised the spectre that more could follow. (This could have had more substance than an ordinary spectre. Groups such as Morgan Stanley and Citigroup were commonly mentioned as being imperilled in the dark days of September and October 2008.) The whole swap market, whose total value ran to trillions of dollars, could fail.

Around the planet, banks stopped lending to each other, because none knew what the exposure of the others might be. All normal credit between banks was frozen.

To cut a long story short, the markets gradually calmed thanks largely to the US government’s intervention on behalf of its banks. Gotterdammerung was avoided, but not by much.4 Since March 2009 we have seen an uncertain recovery in the USA and Europe.

The bailouts cost the US taxpayer dearly. The US government gave Bank of America $US20 billion before its merger then another $US25 billion to prop up the merged group. Despite these injections, Bank of America was still sick, losing $US15 billion in the last quarter of 2008. The US Secretary of the Treasury, Hank Paulson, pressured the Merrill Lynch board into keeping the losses secret until their shareholders approved the merger, which meant Merrill’s shareholders granted $US50 billion of their stock to shareholders in the Bank of America when that bank was arguably worth zero.

AIG cost even more. The US government first spent $US85 billion on warrants giving it a 79.9 per cent stake in the insurer. That wasn’t enough so the government pumped in another $US38 billion. Eventually a total of $US441 billion had to be provided to keep AIG solvent.

Those bailouts were dwarfed again by the Troubled Asset Relief Program (TARP), under which the Federal Reserve committed $US1.25 trillion to buying mortgage-backed securities from its investment banks.

At present the US economy is supposed to be in recovery. By traditional yardsticks, however, this seems dubious. The government has been severely stretched by its support of failing banks. The Federal Deposit Insurance Corporation at the end of 2009 slipped into negative territory for only the second time in its history, with a balance sheet in deficit by $US15 billion. By September its list of problem banks had climbed to 829 with some $US403 billion in assets.5

Between January 1, 2008, and October 1, 2010, a total of 297 banks had been put under the FDIC’s administration. The states which experienced the most bank failures were Georgia, with 44; Illinois, 36; California, 32; Minnesota, 14; Washington, 13; and Nevada, 10. So now you know where to find the dopiest banks in America. Good hunting.

Perhaps the most worrying bank is the Federal Reserve. While several of the investment banks it rescued have now repaid their debts, the Fed has been left lumbered with their toxic waste. Income from the mortgages that is in excess of their financing costs is transferred to the US Treasury to help reduce its deficit. But if interest rates rise, the value of the Fed’s portfolio will be undermined.

At October 1, the Fed’s balance sheet looked like this:

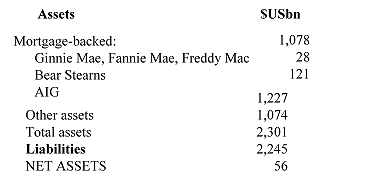

The assets classified as “other” are the normal financial assets of a central bank and are readily liquid. The mortgage-backed assets are classified as taking ten years or more to be liquidated. There have been optimistic reports recently that the Fed is hoping to sell bits of its AIG exposure, refloat what is left of the group and scramble out of its AIG investment square.

Good luck if they can, but meanwhile that is a horrible balance sheet. If these were the accounts of any normal bank it would be judged insolvent, but the Fed is backed by the world’s reserve currency. For an interesting article on the Federal Reserve, go to Google and type “Federal Reserve DV01”. That will give you a discussion by an analyst named Alan Boyce in March 2010, in which he has calculated the impact on the Fed for every basis point movement in interest rates. Boyce currently works for George Soros, who may well have a short position on the $US, but even after allowing for bias the article makes grim reading. Boyce reckons that for every 0.01 per cent move in interest rates, the value of the Fed’s toxic waste changes by between $US1 billion and $US1.5 billion.

A fall in interest rates improves the value of the portfolio, but as US interest rates are already near zero, that is unlikely. An increase of 1 per cent in interest rates, however, would decrease the value of its portfolio by between $US100 and $US150 billion. So the Fed is unlikely to increase interest rates soon. Which means that the USA has lost the use of monetary policy as an economic tool.

In October 2010, the expression “QE2” came into vogue in Washington. That was not a reference to Her Majesty, but stood for Quantitative Easing (Strategy 2), and meant that instead of effecting monetary policy through the interest rate, the government was planning to reflate the US economy by printing money. That will trash the $US in currency markets, but may help stimulate the economy and alleviate unemployment. It may, but use of the printing press to solve economic difficulties has a long and dubious history from the Weimar Republic in 1923 to Robert Mugabe’s Zimbabwe.

The US would not appear to have much control over fiscal policy either. The last US budget deficit was $US1.4 trillion. (Until the last two years, the only times I had seen the word trillion used in actual measurement, it related to astronomy or natural gas reserves. To put the number into some sort of perspective, a trillion seconds is 31,709 years.) If the USA did not print the world’s reserve currency, the IMF would be walking over it in hobnailed boots.

Time to address the question we started with: Could the GFC happen again? In my opinion, the answer must be “Yes” as far as the USA is concerned.

In July 2010 the Dodd–Frank Wall Street Reform and Consumer Protection Act was signed into law by President Obama, who declared it the most sweeping set of reforms since Franklin D. Roosevelt’s New Deal. Considering that most of the so-called reforms since Roosevelt have consisted of unshackling Wall Street, Obama was probably right, after a fashion.

To a cynic the legislation—largely written by Geithner—is fairly modest re-regulation. The law gives the government authority to take over and liquidate failing financial firms. That will not, of course, stop them from failing.

It creates a Bureau of Consumer Financial Protection with a budget of $US500 billion which is expected to recruit an army of examiners to scout the banks for malpractice. The new law is supposed to make derivative transactions more transparent and to restrict banks from making risky bets. Only time will tell how effective these measures will be against financiers and bankers who have a long history of sliding past the letter of the law, or having the law changed to suit themselves.

The outrageous salaries and bonuses have been left untouched. The government could not even control the behaviour of Merrill Lynch and AIG in this respect, despite injecting half a trillion dollars into those two basket cases.

The Merrill Lynch–Bank of America merger had barely been approved when Merrill’s chief executive John Thain disclosed that the group was handing out $US3.6 billion in bonuses to directors and management. Nor was AIG’s management inhibited by the massive bailout. AIG’s executives treated themselves to lavish golf courses in California and a luxurious shooting trip to Britain.

On my analysis, the prime causes of the GFC were:

1. The disconnection of mortgage originators from mortgage holders

2. Allowing investment banks to become public companies

3. The repeal of Glass–Steagall

4. The mushroom growth of unregulated derivatives trading, and

5. Allowing investment banks to become too big to fail.

I see nothing in Dodd–Frank that directly addresses any of these issues. Even if it did, the recent history of financial regulation in the USA has been unimpressive, to say the least.

US banks have been behaving recklessly for decades. Attempts at tougher legislation—to control the derivatives market, for instance—have been thwarted by the banks’ formidable lobbying powers in Washington. There have been repeated failures of banks and major financial institutions since the collapse of Penn Square in Oklahoma in 1982. There have also been repeated bailouts by the federal government, most notably after the savings-and-loans disasters of 1988, when the cost to the US taxpayer was $US125 billion.

Scandalous, even criminal, dealings have been uncovered but no major banker has gone to jail or even suffered a significant penalty. Instead, the men who run the banks have continued to pay themselves fortunes, which were too often undeserved. These patterns of behaviour have become so ingrained that it seems unlikely Dodd–Frank will much inhibit them. Nor is there any sign that the men at the top of the US investment banks have any contrition about the chaos they have caused.

For all these reasons, it is probable that as soon as the bright, immunising memory of 2008 has dimmed—and it’s getting fairly dim already—the USA will have another financial crisis of some kind.

The question then becomes whether the misdemeanours of the US banks will again infect the rest of the world. That will depend on whether the rest of the world is silly enough to keep buying whatever the US banks are selling.

Trevor Sykes is the author of a new book on the GFC, Six Months of Panic (Allen & Unwin, $49.99). Creator of the Pierpont column in the Australian Financial Review, Sykes has studied both current and historical financial disasters for more than forty years. His other books include The Money Miners, Two Centuries of Panic, The Bold Riders and Operation Dynasty.

Notes:

1. William D. Cohan, House of Cards, page 294. House of Cards is an excellent account of the fall of Bear Stearns. Cohan is quoting from an article by Dennis Sewell in the Spectator.

2. This is an actual example from a Series II Mahogany note issued by Lehman Brothers in Australia. The example is given on page 95 of Six Months of Panic by this author. The Mahogany notes went into default, not because of defaults by the entities it contained, but because of the default of Lehman.

3. The Big Short, footnote to page 171.

4. Australian Financial Review, September 20, 2010.

5. To see how close we came, the best book is Hank Paulson’s On the Brink.