Sign In

Sign In 0 Items (

0 Items ( Search

Search

The Morrison government is in a world of pain and, with Malcolm Turnbull exercising his malevolence behind the scenes, things are apt to get worse — unless, of course, the Coalition can craft policies that will take the fight to Labor, rather than complacently acquiescing to the foe’s agenda. My purpose here is to demonstrate just one example in which the government can turn what appears at a glance to be a Shorten vote-winner into a negative.

The Morrison government is in a world of pain and, with Malcolm Turnbull exercising his malevolence behind the scenes, things are apt to get worse — unless, of course, the Coalition can craft policies that will take the fight to Labor, rather than complacently acquiescing to the foe’s agenda. My purpose here is to demonstrate just one example in which the government can turn what appears at a glance to be a Shorten vote-winner into a negative.

To be frank, in view of recent developments including the punishment being inflicted on Jim Molan and Craig Kelly for the crime of holding traditional Liberal views, I no longer much care about a party that knows not its own mind, let alone that of the electorate. But old habits die hard and I have always hated to see specious and facile claims go unchallenged. The issue of negative gearing is my case in point.

Compared to the devastation Labor will inflict on our economy at large – particularly in the sectors exposed to crippling and quixotic warmist initiatives – the issue of negative gearing is probably not a first-order concern. Nonetheless, it does merit some attention. While Labor presents negative gearing as part of its ‘politics of envy’ strategy, the government is failing to counter that narrative by not fully explaining how negative gearing works and the benefits flowing from it. Let me try to redress that failure.

The very term ‘negative gearing’ suggests some dodgy mechanism to evade paying tax and Shorten & Co play subtly on this theme. But the first point to make is that genuine investors of any kind do not set out to make a loss; they want a return on their investment. The second point to make is that investment in property is designed to accumulate personal wealth, which the party of Menzies has always held to be a good thing. The third point is that all wealth, other than the inherited sort, is built on borrowing.

Rental properties are investments like shares, bonds or avocado farms. Rental-property receipts are treated like any other income (eg share dividends) and are taxable. By virtue of negative gearing, they are treated the same as the latter: profits are taxable and losses tax deductible. If legitimate investments why should that not be the case? Why would economists, even Keynesian ones, cheer measures designed to reduce the value of an asset, which is what Labor’s policy would do.

The fundamental questions concern whether residential housing is a legitimate investment, or is there some higher social need that should see it removed from the strictures of the free market?

Two propositions are most often advanced for removing negative gearing. First, it is often stated that it allows rapacious investors to snap up housing to the detriment of first-home buyers, well-heeled investors being in a position to outbid the would-be owner occupier; therefore negative gearing needs to be curtailed or eliminated in order to satisfy the national aspiration to own one’s home. At what price point does negative gearing switch from being a good thing to an evil that must be curtailed by legislated fiat?

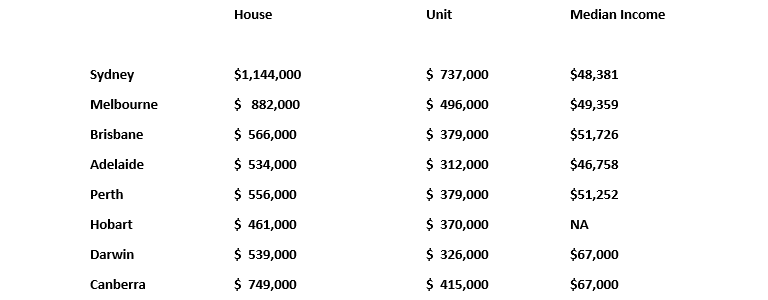

But do property investors really drive up the price of residential housing? This meme is being driven by the fact that housing prices in Sydney and Melbourne have sky-rocketed in recent years. But if property investment were to blame, why wouldn’t we see the same phenomenon in every other capital city? The table below is from Domain’s June 2018 report, and median incomes according to Melbourne University’s HILDA report for 2018 (Hobart was not included in this report and Canberra and Darwin were joined):

We are told that approximately 7% of Australians ‘negatively gear’. Assuming that these investors are spread uniformly across the country, what the table above tells me is that, essentially, prices are high in Sydney and Melbourne because that’s where the bulk of people want to live and supply has not kept up with demand. Cynics might add that prices are high in Canberra because it is full of overpaid bureaucrats.

The second anti-negative gearing proposition, according to Comrade Shorten, is the way in which it allows fat cats to rip off the taxpayer. If you look at Labor’s policy, presented under the headline “Positive plan to help housing affordability”, the emphasis is on increasing revenue by the removal of tax concessions which, in true Wayne Swan mode, are called ‘tax subsidies’. Here’s a sample:

Tax subsidies are skewed to high income earners. Australians benefits from the Commonwealth through either the payments or the tax system. The OECD and the Henry Tax Review has recognised that payments are highly targeted in Australia, and overwhelmingly support low income Australians. However tax subsidies are highly inequitable, with the vast majority of benefit to high income earners.

For negative gearing, the top 20% of income earners receiving around half of the negative gearing benefits, according to NATSEM. The top 10% capture more benefit that the bottom 60%.

In February, then-treasurer Scott Morrison told the National Press Club:

“Two-thirds of those who use negative gearing have a taxable income of $80,000 or less. Seventy per cent own just one property, and 70 per cent have a net rental loss of less than $10,000”.

To me, the central message is that negative gearing is a tool not only available to those of relatively modest means — teachers, policemen, nurses and the like — it is, in fact, being used by them. In other words, negative gearing is not the exclusive preserve of the rich, contrary to Labor’s claims.

Here’s how the ABC’s Fact Check Unit responded.

Mr Morrison’s claim is selective.

Australian Tax Office data shows that one in 10 Australians who files a tax return is negatively geared in terms of rental property. Data provided by Mr Morrison’s office, based on Treasury calculations, showed 67 per cent of the people who use negative gearing have taxable incomes of $80,000 or less. This was backed up by Fact Check’s analysis of ATO statistics.

So Mr Morrison’s claim is correct. But the ABC being what it is, there is also this qualification:

However, as 82 per cent of all taxpayers have taxable incomes below $80,000, it is not surprising that most of the negative gearers fall into this category.

If you believe Labor’s hype, it is surprising.

As this category represents only 67 per cent of negative gearers, it is clear that these taxpayers use negative gearing proportionately less than taxpayers with higher income.

Since people with incomes below $80,000 include many whose incomes are so low they pay no net tax and therefore would not have the wherewithal to invest in property, it is not surprising that proportionally more of higher income earners use negative gearing.

Put another way, only 8 per cent of people with taxable incomes less than $80,000 use negative gearing, compared with more than double that proportion among people with taxable incomes above $80,000.

Fact Check used Professor Miranda Stewart of the Tax and Transfer Policy Institute of the ANU to help discredit Morrison. Here is a gem from her:

Professor Stewart told Fact Check that average male full time earnings were about $82,000. “I don’t think average full time male earnings is modest,” she said. “By definition it’s average and much higher than many workers get.”

She says that median income of about $52,000 is a more meaningful basis to assess the fairness of negative gearing. Fair enough. The Fact Check report then goes on to say that only 40% of negative gearers are in the $52,000-or-below cohort. Only 40%? That seems a pretty respectable figure to me.

Finally:

Fact Check’s analysis showed that 70 per cent of negative gearers had rental losses of $10,000 or less.

The low rental losses claimed by the majority of negative gearers show that most are not gaining a significant benefit from negative gearing.

That’s also what Morrison claimed and hardly supports the idea that rich investors are ripping off the taxpayer. And, by the way, that last statement holds true only if the primary purpose of negative gearing is tax avoidance or tax minimisation.

Let’s have a look at a couple of negative gearing case studies. Let’s say I’m earning $80,000 and I pay a top marginal rate of 32.5c in the dollar. So before any deductions, I pay $17,547 income tax. (For the purposes of this example, I’ll ignore all other deductions.) Let’s further say that I manage to save $300,000 and use that for a deposit on a rental property worth $800,000. I need to borrow $500,000 and secure an interest-only loan over 30 years at 6%. (In reality, I wouldn’t maintain an interest-only loan over such a long period but would pay down principal wherever and whenever I was able.)

Let’s say I get $600 per week rent, $31,200 pa. I am paying $30,000 p.a. interest on my loan. That is tax deductible. I pay annual property rates of $2,000 and insurance of $1,000, plus I engage a managing agent who charges, say, 10% or $3,120.

My outgoings are $36,120. So I’ve made a loss of $4,920. My taxable income is now $75,080 and tax payable is $15,948. So I’ve “ripped off” the government to the tune of a measly $1,599 – considerably less, I would guess, than the average low-income worker draws in various benefits and subsidies. And keep in mind that in order to achieve this tax saving of $1,599, I’ve had to fork out $4,920 in interest payments. That’s come out of my take home pay. Day to day I’m living on less than I otherwise would have — $126 per fortnight less to be exact.

So getting back to those ‘negative gearers’ with losses of $10,000, in my case I would need two investment properties leveraged as above and my out-of-pocket expense would be $6,642 and the loss to taxpayers would be only $3,200. Not $10,000 as some might infer from Morrison’s statement.

But what about those high-income earners? Just how rapacious is the ‘speculator’ class? Fortuitously, a perfect example presented itself a year or so ago in the person of one David Feeney, one of Labor’s own stalwarts and the then-member for the Melbourne seat of Batman who failed to declare on the Register of Pecuniary Interests a rental property worth a reputed $2.3 million in the trendy Melbourne suburb of Northcote. Feeney told us the property was rented at $700 per week and that it was negatively geared. As an aside, an annual return of $36,400 on capital of $2.3 million does not strike me as a particularly savvy or fruitful investment. Thank goodness Feeney never got his hands any of the financial levers available to government.

I don’t know exactly how much Feeney pocketed as an Opposition frontbencher but, for the purposes of this exercise and ease of calculation, let’s use $200,000 (MP base salary is $193,000). That puts Feeney in the top tax bracket. On $200,000 he would pay $63,547 p.a. income tax. Let’s further assume he borrowed $1 million on the property. His annual interest bill, again based on interest at 6%, would be $60,000.

Let’s again assume rates and insurance at $3,000 p.a. and agents fees of $3,640, giving total annual expenses of $66,640. Feeney’s annual loss would be $30,240, leaving him a taxable income of $169,760. On this he would pay $50,758, saving himself $12,742 p.a. and leaving him $17,498 out of pocket.

Let’s now imagine Feeney were a more canny investor than he appeared to be and outbid me for the same notional $800,000 property that I mentioned earlier, and that he also borrowed the same amount ($500,000). His annual loss, not surprisingly, would be the same: $4,920, reducing his taxable income to $195,180. He would now pay tax of $61,634, a saving of only $1,866, and be $3,054 out of pocket. A result virtually indistinguishable from mine.

In pushing its anti-negative gearing line, Labor often cites a hypothetical high income earner with ten negatively geared properties. There may be a such investors, but you can bet they won’t have 10 properties all as highly leveraged as in my examples. But, even if they do, the tax advantage they receive will be neither here nor there in the grand scheme of things vis a vis total government debt.

And keep in mind that these figures are based on interest-only loans. In reality, the serious property investor will also pay down principal while seeing his rental income increase over time, thus reducing the annual loss. In other words, in the examples quoted above the tax savings at the start of the loan are as big as they get. As principal gets paid down the losses decline.

In case you haven’t already got it, my point is that serious property investors, if they are honest, are not doing it to minimize tax. They are doing it to accumulate wealth. I’m willing to bet that property investment, kick-started by negative gearing, has been hugely more successful than superannuation at keeping people off the age pension.

Right now the Age Pension costs us about $50 billion per year. Universal superannuation was supposed to help rein in this figure, which it has signally failed to do. If anything we should be encouraging more people to invest in property. And, of course, superannuation contributions also attract ‘tax subsidies’. The reasons why wealthier taxpayers ‘benefit’ more from negative gearing than middle or working class families are because they have more disposable income and they pay higher rates of tax. But the fact that they do proportionately better is hardly a good reason to deny the less well off the same opportunity. This is nothing more than the politics of envy on steroids.

But what about Labor’s policy? They claim it will ‘make housing more affordable’. They have produced modelling to prove it. The government has cited modelling that proves it will decimate the real estate market. By now, we all know that there is wishful thinking, damned wishful thinking … and modelling. When it comes to duelling models, the one that underpins the slickest snake oil will prevail in the public mind. It is hard to see how restricting negative gearing to new properties will give first home owners a better shot at their dream. Won’t investors also target these properties? Labor’s policy is incoherent, except when viewed as a thinly disguised tax grab.

So what can the Liberals do? Well, for a start they could respond to Labor’s policy by packaging up a new policy of their own, promoting the concept of property investment (with negative gearing as one incentive) as a mechanism for long-term financial independence. They could encourage first home buyers to take advantage of the scheme by, for example (and this is just a thought bubble), restricting the sale of Defence Housing properties to first home buyers. DHA properties are a very good investment with guaranteed income. They could subsidize such sales by picking up the tab for stamp duty. They could negotiate agreements with state governments to extend the first home buyers grant to such sales.

They could also tighten up the regime by banning interest-only loans and ensure that the ATO cracks down on infractions where, for example, properties are let at well below market rates or left untenanted for long periods. I doubt much of this goes on but it’s good window dressing to counter the inevitable Labor counter attack. Government might also (another thought bubble) entirely waive capital gains tax on properties (it is now 50% on those held more than a year) sold after owners reach retirement age, cutting down on speculation.

And, perhaps most potently, they could shout from the rooftops that even economists openly sympathetic to Labor are now saying the planned assault on negative gearing is a lunacy in light of the downturn in Melbourne and Sydney property prices. Here, for example, is Michael Pascoe writing in the left-wing, union-funded New Daily:

The current correction in Sydney and Melbourne housing markets is unlikely to be over. Investor interest has already been curtailed by regulator-enforced credit tightening and many investors having the brains to realise the party is over for the time being.

Those two factors have reduced the need for restricting negative gearing…

Sadly, riven as it is by factional discord and harbouring political malignancies who really belong in some other party, the Liberals have only a half measure of the wits needed to mount a persuasive and coherent counterattack. If Labor gets in, as seems likely, and sticks to its class-war policies, brace yourself. It won’t be pretty.

Sigh …

Super was never designed specifically to keep people off the age pension (although in my case, that is exactly what has happened). It has the other design of reducing the age pension payable or postponing the age at which an age pension may be applied for, so reducing the impost on the public budget.

Compulsory super is a little over 25 years old, just 63% of the design life deposit period of about 40 years, ie. from one’s mid-20’s to mid-60’s. With almost 40% of lifetime deposits to go, it is deliberately dishonest to call *failure* this early. Both Judith Sloan and that Creighton have been running this dishonest line for months now. O’Brien has just joined them.

I don’t understand O’Brien’s and Sloan’s motives here. Creighton, as a millenial ex-Treasury person, is simply regurgitating the Treasury view that the “concessional” tax that is applied to super really belongs to them.

My motive is clear. Super represents a clear path to some independence in old age. That Governments, politicians, bureaucrats, “wealth” managers, banks, union mates, life insurance, Uncle Tom Cobbley et al can all have a go at it over the 40 year period while the poor sod who deposits and deposits and deposits under duress cannot touch it for those 40 years is the fault of greedy authorities, not the concept of super per se. These despicables simply cannot keep their hands off other people’s money.

Greed and dishonesty, hidden agendas, contempt for the little people. Is ever thus … remember the Cyprus bank crash, wherein the banks were recapitalised by purloining, expropriating (stealing) huge chunks of people’s pension savings. This left older people, either out of the workforce or on the verge, destitute.

Ianl, you must not have read my article very thoroughly. It is not about trashing superannuation but about dispelling the myths that Labor have been peddling about negative gearing. I see real estate investment as a complement to superannuation to maximise retirement savings.

All those mum and dad businesses who support their operations by using the family home to provide equity as security for banks.

What of them when Short-on-brains gets the keys to Kirribilli?

As their property prices tank, banks will tighten (even further than they have to date) starving SME of the funds to expand, create employment etc.

It’s almost like Shorten has no grasp of “unintended consequences” as a concept.

‘Myths about negative gearing?’

Pete; you have reinforced my judgement re the political leanings of this forum.

Why should anybody be entitled to a tax benefit for deliberately engineering a financial loss situation?

Also; the First Home Buyers Grant was just a political bonus for the real estate industry, gifted by both Federal and State Governments. It just inflated the market, is rorted enormously and is a counter-productive imposition on government budgets.

It is mindless folly to rely on the property industry as a main leg of economic activity.

Abolishing both negative gearing and the FHBG would be positive moves toward stabilizing the property market in Australia.

Bushranger71. Why would you imagine people want to lose money for longer than they have too? Properties move pretty quickly to a positive income, took 2 years for mine to do that.

Since then, the write-off of losses in the early years against other income has been eclipsed multiple times by taxes paid on the subsequent earnings and I will stump up 50% of the capital gain if~when I sell it.

How is that an issue?

Oh here is a tip. If you stumped up $68 and were not aware that this is a conservative-leaning magazine then you have been living under a rock.

Okay Rob; it worked for you in a buoyant market. Did not negative gearing (and unfettered immigration) have some influence on soaring real estate prices?

It does not look so good now of course with prices declining and probably falling appreciably further.

In response to an email from Keith Windschuttle, I will shortly let all know exactly why I will not be renewing my subscription to Quadrant Online.

He errs in nailing a political flag to the masthead and QOL typifies just what is wrong with debate in Australia these days.

By the way; I was formerly a member of the National Party and have voted Informal since 1996 because I feared what John Howard would do to Australia.

Bushranger 71, you too have failed to understand what I have written. Your response is just a strawman argument. I never claimed that someone should be rewarded for ‘engineering a financial loss’ Quite the opposite in fact. And over the long term, real estate is a a solid, if unspectacular, investment.

Some countries do not allow this tax offset between an income and a totally unrelated investment loss!

Maybe the government could reduce the scope of the domestic rental negative gearing to one property only. This reduction of the scheme may be resented by the many parliamentarians from both sides who take advantage of the scheme to pay no tax while acquiring multiple properties.

It is reported that the Liberal defector Julia Banks lives in a $3 million house and has 4 investment properties!

Brandee, what is your objection to investment in residential real estate? Is there a limit on how many companies you can buy shares in? Does the fact that Banks is a sleaze automatically discredit anyone who owns rental property? And you have totally misunderstood the thrust of my article or chosen to ignore it. As Rob Brighton has pointed out, done properly, losses are small, over time they diminish to zero and tax becomes payable. And, as I have pointed out, it is not only MPs who invest in rental property. Your comment just echoes the Labor politics of envy line.

Bushranger71 You realise there is real estate outside of Sydney and Melbourne? Try reading this and you will see your assumptions are wrong. https://www.warringalfs.com.au/static/uploads/files/adelaide-capital-city-review-edition-2-2016-wfgdtzczkefr.pdf

All that aside, there is an underlying principle that Mr OBrian spoke of in his article. That is everyone is taxed on their total income, not just those parts that are making profits (this also leads into Short-on-brains raiding superannuation franking credits)

Change that for just the real estate market and you will distort a huge part of AU’s economic activity which is perilous, to say the least.

Brandee:- How is it unrelated when the income is earned by the same person?

@Peter O’Brien

> “Ianl, you must not have read my article very thoroughly”

Oh yes I did. I specifically included at the beginning of my comment a quote from your article which disappeared from my published comment. I’ll include it again, although I do NOT trust this new website to faithfully include all one says:

> “I’m willing to bet that property investment, kick-started by negative gearing, has been hugely more successful than superannuation at keeping people off the age pension”

That’s what I objected to – the silly flippancy.

[As an aside, I object to the lack of nested reply ability in this “new” website, the removal of double spacing between paragraphs and the seeming dropping of parts of comments. One is constantly dunned for contribution to QoL but is presdented with a dumbed-down facility. Not conducive]

Ianl, no flippancy intended. I stand by my comment. 80% of retirees are on full or part pension. We are told between 7% and 10% of Australians invest in real estate. Do you think 80% of them are on full or part pension? I don’t.

It’s a good article, Peter, but Ianl has a point, and your rejoinders to him are weak. People who negatively gear are overwhelmingly younger and still working, with another source (or sources) of income to negatively gear against. Retirees, however they are financed (from their lifetime savings, the age pension or some combination of the two), are most unlikely to be negatively gearing any income-producing asset, let alone real estate.

Since Keating, everybody has had to contribute compulsorily to super, and reforms under Costello encouraged voluntary saving for larger super balances. This was clearly producing a huge swing away from dependency on the full age pension to transitional receipt of only a part age pension.

It is customary to mock that change as inadequate, but when realistically modelled over the 40 or more years it takes policy changes to produce effects in lifetime savings, it was a good policy. (see https://treasury.gov.au/publication/modelling-the-sustainability-of-australias-retirement-income-system/ )

Then the witless Liberals destroyed it and opened the floodgates for Labor to continue to pillage super balances into the future, as Grattan is now recommending.

Tezza, although I am a retiree and no longer in wealth accumulation mode, my article was not directed at retirees. The whole point of my article is that acquisition of real estate is a very effective means of acquiring wealth. It should not be allowed to be disparaged by specious politics-of-envy rhetoric against ‘negative gearing’ which, in fact, is nothing more than a tax deduction that applies to any other investment. My article touches only very peripherally on superannuation. In the end it may turn out to be fantastic but we will have to wait and see.